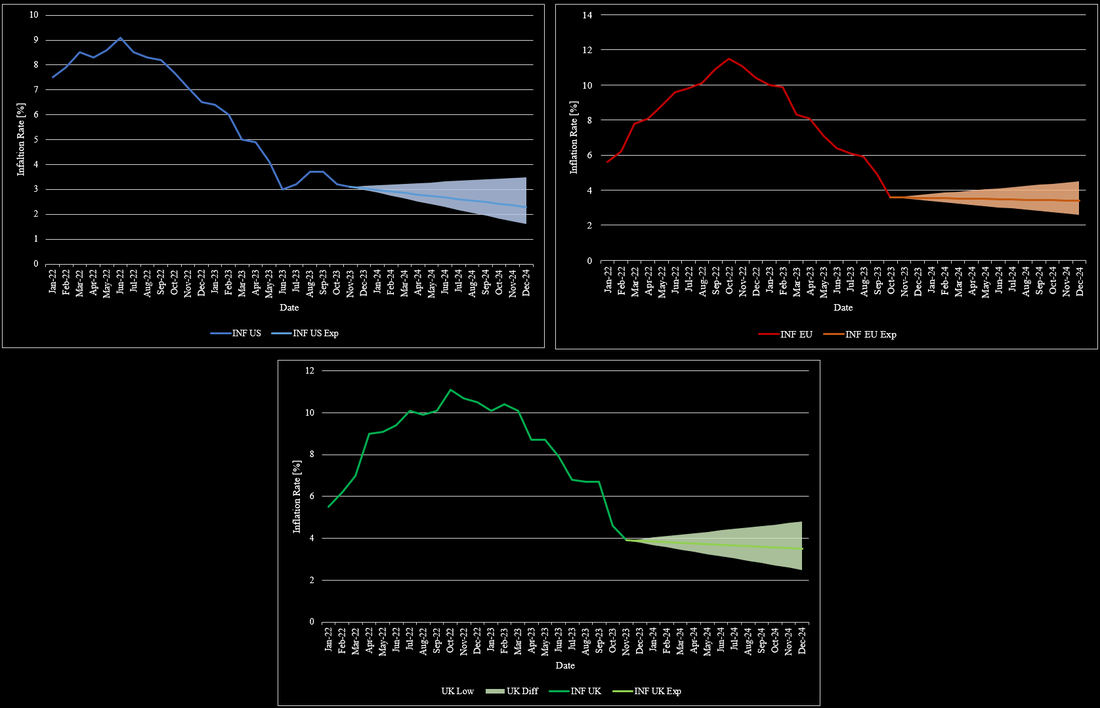

Inflation remains a key contributor to global risks, particularly in the US. Since June 2023, inflation has fallen below 4%. While this initially looked promising, inflation has never fallen below 3% and remains sticky. As a result, most market participants expected the Fed to cut rates several times during 2024. Recent developments have changed these expectations dramatically. At its most recent meeting, there was a significant chance that the Fed would even raise rates again. At its meeting in early May 2024, the Fed is holding its rate between 5.25% and 5.5%. While rate hikes are less likely in the near term than before the May meeting, some economists do not see a cut before 2025. Whether interest rates are lowered is increasingly dependent on the US labour market. With its current strength, the economy can tolerate higher interest rates. If the labour market shows signs of trouble, cuts are likely to come sooner than expected. While inflation will remain a key criterion for such a decision, the focus seems to have shifted to the labour market. Figure 1 shows the development of inflation and interest rates in the US, the EU, the UK, and Switzerland.

In the EU, inflation has been on a healthier decline. Inflation in the EU has fallen to 2.6% in March 2024, the lowest level since the start of the inflation spike. Interest rate cuts now seem much more likely in Europe than in the US. Even in the UK, inflation is coming down to manageable levels and the BoE has hinted at earlier cuts than previously thought. Switzerland, which has been unique during soaring inflation, was even able to already to lower its interest rate from 1.75% to 1.5% in March 2024.

The hedge fund industry has been experiencing a consolidation trend for many years now. However, in contrast to the past few years, never was it as pronounced as in 2023. In fundraising terms, smaller hedge funds struggled to raise sufficient capital throughout 2023, while large hedge fund managers saw huge inflows and even extended their offered funds. This effect was especially notable as the industry saw redemptions of a total of $280bn in 2023, as shown in Figure 1. When separating inflows into top-ups and new investments, top-ups dominated over the past three years, which again highlights the strength of established and emerging managers. In 2023, most established managers also were able to generate solid double-digit returns for investors, which is certainly appealing to investors. It is somewhat surprising that there is such a strong tendency towards large and established managers, as it is widely known that these managers charge (substantially) higher fees than other funds. 2023 was also an extreme year in terms of fees, as some of the largest managers keep more than 50% of the gains for themselves and the remainder flows to the investors. This emphasizes the strong preference of investors towards established managers. The reputation and the “proven skill” of these managers provide investors with a certain degree of “safety” when investing in hedge funds.

2023 followed the core theme of 2022 with a key focus on inflation and interest rates. At the beginning of 2023, inflation was a huge concern, due to its high level. In the US, inflation was at 6.5% and already declined substantially from its peak in June 2022 at 9.1%. This trend continued in 2023 until it reached its bottom in June 2023 at 3%. Since then, US inflation remained steady between 3% and 4%. The EU and the UK saw a very similar development of inflation throughout 2022. Their respective inflation started at around 5.5% in January 2022 and rose to 10.5% by the end of 2022. As soon as 2023 started, inflation in the EU started to decline and eventually declined to as low as 3.1% in November 2023. Despite this promising development, inflation began to increase again to 3.4% in December 2023. While the UK’s inflation development was almost equivalent to the EU’s in 2022, this changed in 2023. Inflation in the UK remained above 10% until April 2023, at which point inflation was at 10% or higher for almost an entire year. Nonetheless, UK inflation also came down later in 2023 and reached the 4% mark at the end of December 2023. Based on the overall relatively similar development of inflation around the world, it is likely that inflation will stay at elevated levels in the short term. Another key reason for relatively stale inflation is that central banks stopped hiking their interest rate for a while now in 2023. Figure 1 summarizes the development of inflation in the US, EU, and the UK.

With the soaring inflation in 2021 and afterward, central banks had to react. Financial markets enjoyed rates close to zero, if not negative, for a long time. As a response, central banks started raising their interest rates. The Bank of England was the first to raise its interest rates in December 2021. The Fed followed in March 2022 and hiked its rate in every meeting and by a higher amount on average than the BoE or the ECB. The BoE did so too, but did smaller hikes on average. The ECB followed in June 2022, but they did not hike at every meeting. At the start of 2023, the interest rate in the US was already at 4.25% compared to 3.5% in the UK and 2.5% in the EU. Consequentially, the ECB hiked more in 2023 but did not reach the same heights as in the US or UK, which are currently at 5.25%, while the ECB’s interest rate remains at 4.5%. With interest rates now higher than inflation rates in each of those economies, most market participants expect interest rate cuts in 2024, especially due to an elevated possibility of a recession ahead.

Inflation and interest rates have been present topics. Inflation rates have continuously decreased throughout 2023 across most economies. While this development was promising, it was necessary as inflation rates went as high as almost 12% towards the end of 2022. In the US, inflation has decreased to 3%-4% in the past few months with no particular direction since then. For 2024, it is widely expected that inflation will decrease further, albeit to a limited degree. Most market participants expect inflation to be around 2.3% by the end of 2024. Others see inflation to drop to as low as 1.6%. Assuming no further geopolitical crises and no further escalation of existing crises, inflation is unlikely to rise further than 3.5% by the end of 2024. Figure 1 shows the development of inflation rates in the US, UK, and the EU from January 2022 to the end of 2024. The general sentiment that inflation rates should fall is intuitive given the high interest rates at this time. In the EU, the development has mostly mimicked the US, but with a delay of a couple of months, due to a more restrictive central bank policy when Covid-19 emerged. Inflation in the EU has also reached a point, where inflation is no longer declining at levels slightly below 4% after being at 10% at the beginning of the year. For 2024, inflation is also expected to further fall, but not to the same degree as in the US. Expectations for inflation in the EU range from 2.6% to 4.5% with the most likely level around 3.4%. The situation in the UK also drastically improved towards the end of the year. UK’s inflation fell to 4% after lingering around the 10% mark for almost an entire year. Inflation expectations for the UK are mostly equivalent to the EU’s expectations, but its projections are more volatile based on the country’s state over the past few years.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |