With inflation remaining high, rates are trading higher than at the beginning of the year. While the view for 2023 is still largely pessimistic, in January the view shifted to more optimism, when most assets posted strong gains. However, this optimism faded to some degree again in February 2023. With inflation only going down slowly, more and more market participants expect rate cuts later than previously expected. This stance is also further supported by the central banks, especially by the Fed and ECB recently. In the US, this led to a substantial rise in longer maturity yields. Nonetheless, the yield curve inversion is still severe. Over the past weeks, yields on 6m- and 1Y-Treasuries have surpassed the 5%, whereas the 10Y-Treasuries are close to the 4% mark. The current yields also are also alarming for the real estate market that now sees a crisis ahead. House prices plummeted since 2020. At least, the impact is not that large as it has been during the global financial crisis, but it could still reach those levels with more time. The now high mortgage rates lead to a strong decrease in home construction. The last time it was this low was back in 1995. The particularly alarming thing is that this is despite the already strongly decreasing house prices. With rates unlikely to go down substantially any time soon, the industry is under significant pressure, which is likely to persist for a while. While the decreasing house prices are substantial, compared to its history, this decline is very small. Since the global financial crisis, the median house price in the US has doubled. In this context, the affordability of housing and in particular construction is at a very low level.

Although 2022 is over, the problems it brought with it are not. Inflation is still high, albeit not at peak levels of 2022. With this development, central banks are likely to stop hiking relatively soon, given that inflation keeps coming down. In the short-term, central banks will continue to hike with some of them reducing the size of the steps. The ECB raised its target rate in early February by another 50bps and announced they will continue to do so. While inflation in the US is better under control than in Europe, they also have their share of problems with a recession on the horizon. Rates are much higher with a lower (but historically still very high) inflation. The US is also facing the largest yield curve inversion since the 1980s, which is persisting for more than half a year by now. In this ecosystem, it is also not surprising that the US reached another peak in its trade deficit. While these developments are somewhat to be expected from the underlying economic situation, the labour market has been as a positive indicator for the entire 2022. In January 2023, the largest job cuts since 2020 was observed. However, this is largely stemming from huge job cuts of big tech stocks, which have suffered a contraction in 2022 after their bull run in 2021. The job cuts are also understandable given that many big tech firms have had their worst or close to their worst growth rate in their history. Similar things can be observed when looking at their revenues. Regarding the unemployment rate in general, it is still very low and there was consistent decline since the beginning of Covid-19. At least this indicator eases some of the pressure of the otherwise highly uncertain economy. In this ecosystem, market participants expect few further hikes with lower rates towards to the end of 2023 and thereafter. With the strong labour market in mind, it would be a great achievement for the Fed to combat inflation effectively without destroying the currently strong labour market. In this instance, it is realistic, as the cause of inflation were the policies applied during Covid-19, most notably the financial stimulus and essentially unlimited borrowing, led to inflow of available of money, which is in itself independent of the labour market. Figure 1 summarizes the expected development of the Fed fund rate until 2025. In the UK, the situation looks a bit more dire. While the BoE has hiked in similar frequencies, it could not combat inflation as effectively as the US. In addition, the UK is more directly affected by the war, which increases the overall pressure on markets. Despite, the BoE substantially adjusted their recession forecast, in which the GDP should only drop by 0.8% compared to almost 3% in their prior forecast. Figure 2 provides an overview of the new and old forecast of the BoE until 2025.

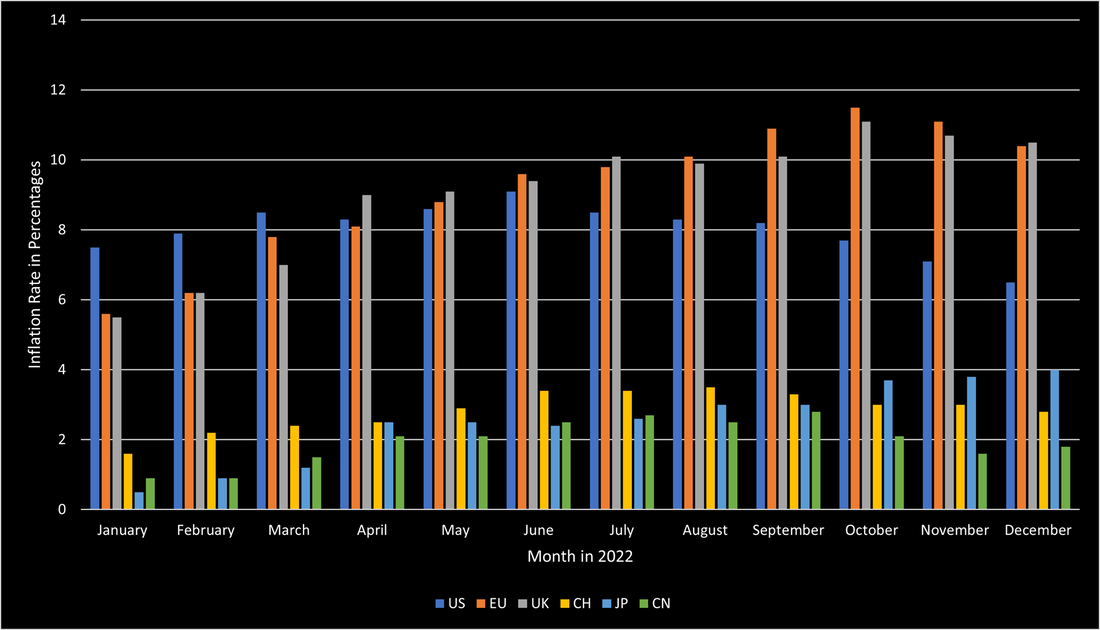

2022 was a year that tested the worldwide economy. The highest inflation in 40 years, unprecedented interest rate hikes, and the invasion of Russia into Ukraine were only some contributors to the hugely difficult year of 2022. In the US, inflation started soaring during 2021 and peaked in the summer of 2022 at 9.1%. Thanks to the central bank’s quick response, inflation has since continuously slowed down and is currently at 6.5%. Europe had significantly more issues handling the inflation crisis. The EU started the year at an inflation rate of slightly above 5.5% and it continued to soar until October 2022 when it reached its peak at 11.5%. The UK was similarly affected, despite the BoE being the fastest-acting central bank to raise interest rates. However, its inflation behaved like the EU’s and soared to its peak at 11.1% in October 2022. Both economies have not been able to reduce inflation below 10% so far. In contrast to the US, European countries were much more affected by the direct impact of the war between Russia and Ukraine. Soaring energy and food prices, for both of which Russia and Ukraine are crucial suppliers, were the main constituents causing the high inflation. Additionally, the ECB did not enjoy as much freedom as the Fed had when raising interest rates. This is in large part due to the high indebtedness of certain European countries that would have gone bankrupt if interest rates would have been raised as much as the US did. Other countries, such as Switzerland, Japan, and China stand out in this discussion, as those countries managed to keep their inflation relatively low. Switzerland managed to avoid such high inflation due to its strong currency, and a limited dependency on fossil fuels. Japan avoided high inflation through the continued quantitative easing by the BoJ. However, in contrast to the other countries, Japan’s inflation is still soaring and poses substantial issues to the country. China avoided high inflation through its rigorous Covid policies and its limited governmental support when Covid emerged. The source of this soaring inflation is a combination of the war but is largely based on unprecedented central bank intervention to save the economy during the early Covid days when large parts of the economy were completely unable to function. Figure 1 shows the inflation levels of the previously mentioned countries during 2022.

ALTERNATIVE MARKETS UPDATE - MID JANUARY 2023 & MACRO AND POLITICAL OUTLOOK 2023 BY MACRO EAGLE11/1/2023

With the currently pessimistic view of 2023, markets are under substantial pressure. Most market participants are expecting a recession in 2023/2024. High inflation, steep interest rate hikes, and historical yield curve inversions are just a few indicators that suggest tough times ahead. However, there are some indicators that provide hope that a larger crisis can be avoided. While inflation is high, it has been steadily decreasing, at least in the US. Rate hikes are also expected to increase only slightly in 2023. Nonetheless, this provides little help in avoiding a recession, as it is still unclear how fast inflation will drop down to the acceptable 2% and below range. Furthermore, interest rates will remain high for 2023 with a low to moderate probability of rate cuts in 2023. These still pressure businesses that are expected to earn less in 2023, as consumers have exhausted most of their resources in dealing with the impact of inflation. The biggest saving grace currently is the labor market, which functions very well. In Western countries, the unemployment rates are close to record lows of the past few decades. In the US and the UK, the unemployment rate is 3.7%. In the EU, the unemployment rate is 6%, while Switzerland sees an unemployment rate of 2.2%. Figure 1 shows the jobless claims in the US in 2022. While there has been some variation during 2022, these were small and at very low levels historically. It is even more promising when addressing the private sector. Since early 2021, the private sector in the US is adding jobs at a constant pace. Figure 2 shows this development.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |