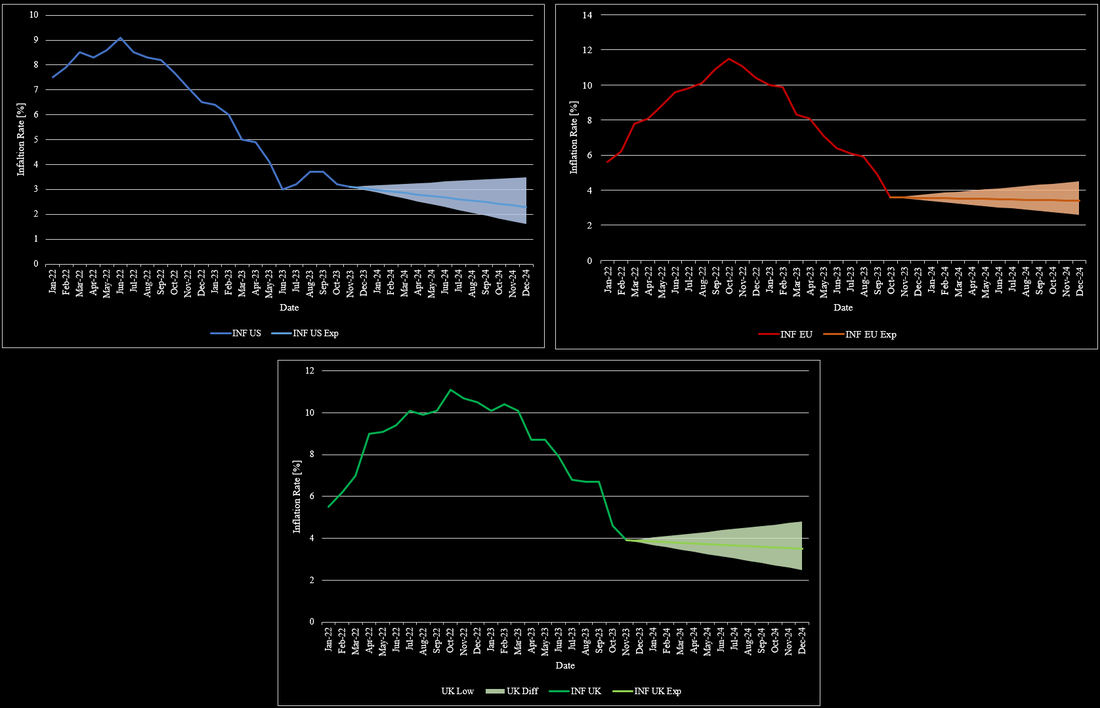

Inflation and interest rates have been present topics. Inflation rates have continuously decreased throughout 2023 across most economies. While this development was promising, it was necessary as inflation rates went as high as almost 12% towards the end of 2022. In the US, inflation has decreased to 3%-4% in the past few months with no particular direction since then. For 2024, it is widely expected that inflation will decrease further, albeit to a limited degree. Most market participants expect inflation to be around 2.3% by the end of 2024. Others see inflation to drop to as low as 1.6%. Assuming no further geopolitical crises and no further escalation of existing crises, inflation is unlikely to rise further than 3.5% by the end of 2024. Figure 1 shows the development of inflation rates in the US, UK, and the EU from January 2022 to the end of 2024. The general sentiment that inflation rates should fall is intuitive given the high interest rates at this time. In the EU, the development has mostly mimicked the US, but with a delay of a couple of months, due to a more restrictive central bank policy when Covid-19 emerged. Inflation in the EU has also reached a point, where inflation is no longer declining at levels slightly below 4% after being at 10% at the beginning of the year. For 2024, inflation is also expected to further fall, but not to the same degree as in the US. Expectations for inflation in the EU range from 2.6% to 4.5% with the most likely level around 3.4%. The situation in the UK also drastically improved towards the end of the year. UK’s inflation fell to 4% after lingering around the 10% mark for almost an entire year. Inflation expectations for the UK are mostly equivalent to the EU’s expectations, but its projections are more volatile based on the country’s state over the past few years.

The month of November has been quite successful for equities and bonds alike. With the stabilizing macroeconomic landscape, markets have adjusted to the current state with high rates and moderate to high, but decreasing, inflation. In the past month, there were promising signs that no more hikes are necessary to combat inflation. A notable percentage of market participants is even optimistic about rate cuts soon. While US inflation has gone down substantially already in summer, European countries are following and are on their way to similar levels as the US. Unsurprisingly, this led to a more positive view on longer-term rates. This was evident in falling yields for longer-term bonds. US and UK 10-year bonds’ yield decreased by around 10% since October, while German 10-year bonds decreased by almost 25%. Figure 1 summarizes the development of 10-year yields from October in the previously mentioned countries.

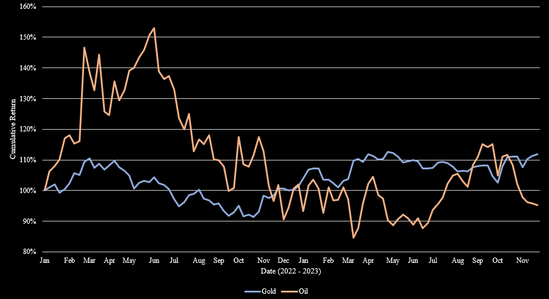

With relatively quiet central banks over the past weeks in terms of interest rate decisions and inflation slowly coming down, financial markets have calmed down with the exception of the impact following the war between Israel and Hamas. The start of the war has reignited interest in gold as a safe haven asset. While gold has been trading close to its historical high throughout the past years, the recent events led to another record high of $2,074 per ounce. After the initial shock from the war, gold declined again slightly, but has since regained most of its value, as the US dollar is getting weaker. Despite high interest rates and positive real rates, gold remains attractive. It is widely assumed that inflation will remain elevated for quite a while. Yet, positive real rates will do so too given that it takes a lot of interest rate cuts by central banks, which will take time. In the medium-term future, gold will not lose its attractivity, due to an elevated crisis risk and the general instability around the world. Since 2022, gold’s price has increased by more than 10%, as shown in Figure 1. While gold remained stable during these times, oil has behaved much more volatile. Compared to the beginning of 2022 WTI crude oil is now down around 5%, despite being up more than 50% in June 2022. Oil strongly soared when the war between Russia and Ukraine started and maintained an upward trend until the summer of 2022. Then, it started to gradually fall to more normal levels. 2023 was characterized by supply cuts to prevent the price from crashing. Further cuts in the summer of 2023 resulted in consistently raising prices for the first time since the war started. The latest war further led to price increases, which stopped the initial downward trajectory, but it was only a brief reaction. Currently, oil prices are still on the decline with the current supply, as industrial demand is slowed. The postponed OPEC+ meeting also contributed to the latest declines.

The conflict between Israel and the Hamas is in full force and it seems unlikely that the situation will be resolved soon. While the conflict started with an attack from Hamas on civilians in Israel, the focus has fully shifted towards Gaza with group, air, and sea retaliation by the Israel military. Israel is strongly focusing on Gaza, as it is seen as the center of the Hamas. The conflict in Gaza is widely seen as a precarious situation, as Israel is completely blocking entry or exit even for vital goods, such as food, water, and medical supplies. While Israel was supported initially by most Western countries (especially due to the many hostages taken), support is continuing to fade, due to the humanitarian crisis it caused in Gaza. Despite the decreasing support, Israel seems determined to not only free all hostages, but also disabling the military and governmental capabilities of the Hamas. Unsurprisingly, the conflict also affected financial markets significantly. While initial price shocks mostly normalized since early October 2023, oil markets could experience further volatility. Additionally, given the already pressured economies, investors move more capital into safe-haven assets, in particular US-Dollar and gold.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |